On March 30th, 2026, the Organization for Cross-regional Coordination of Transmission Operators (OCCTO) released the “Aggregation of Electricity Supply Plans” for FY2026, a compilation of electricity supply plans submitted by 2,234 electric utilities. The compilation shows the electricity companies’ plans for supply of electricity and the development of power sources and transmission lines for the next 10 years, showing estimated results for FY2025 and short- and long-term forecasts up to FY2035.

The plans for FY2026 are especially noteworthy because the updated plans clarify the status for the critical years of 2030 and 2035, which provides insight for future changes in coal-fired power and renewable energy industries. However, the plans reveal the lack of progress towards phasing out coal-fired power. The details of the situation are explained below. Japan urgently needs to revise policies fundamentally in order to overcome the reliance on thermal power.

First, it is necessary to review the international positioning of coal-fired power plants.

(0) International positioning of coal-fired power plants

The following international targets and agreements exist for coal-fired power.

・Developed countries must phase out coal-fired power by 2030

(Proposed by the International Energy Agency (IEA) in its Net Zero Roadmap)

・G7 members commit to phase out existing unabated* coal power generation in their energy systems during the first half of 2030s or in a timeline consistent with keeping a limit of 1.5°C temperature rise within reach, in line with countries’ net-zero pathways.

(Japan agreed at the G7 Ministers’ Meeting on Climate, Energy and Environment in 2024)

*According to the IPCC, unabated coal power under the international agreement means “not adopted emission reduction measures” and it refers to plants that have not implemented measures to reduce or capture 90% or higher of CO2 emissions.

To mitigate climate change, Japan must also urgently advance the phase-out of coal-fired power.

Here are the highlights of the Aggregation of Electricity Supply Plans for FY2026.

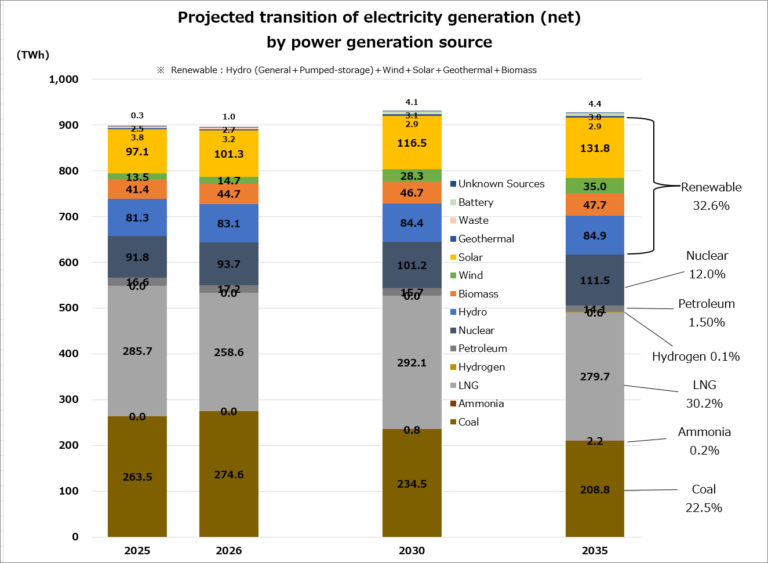

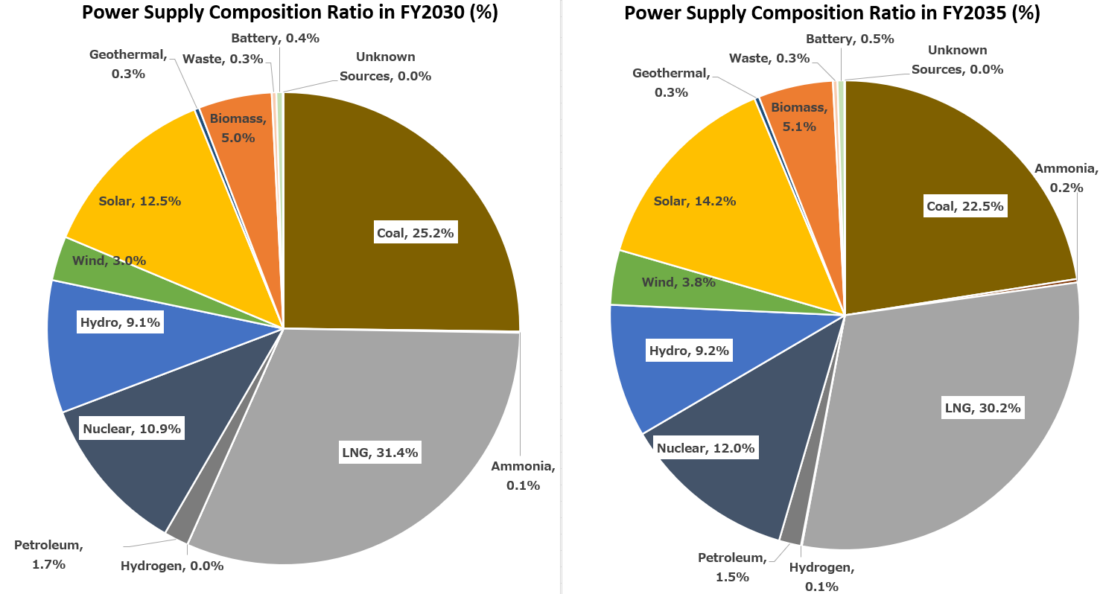

(1) Energy mix: Coal still remains at 23% in 2035

Looking at the energy mix, it has become clear that the serious reliance on fossil fuels is expected to continue. The graph top of this page presents the data for FY2025 and forecasts for FY2026, FY2030 and FY2035.

The graph above shows that coal-fired power will remain at very high percentages, 25.2% in FY2030 and 22.5% in FY2035. LNG-fired power generation also remains as a large proportion, as 31.4% in FY2030 and 30.2% in FY2035. On the other hand, the percentage of coal and LNG-fired power by FY2030 in Japan’s 6th Strategic Energy Plan set in 2021 were 19% and 20% respectively.

In other words, under the current plan, not only will thermal power substantially exceed the FY2030 target, but there is also a high possibility that the FY2030 target will not be achieved even by FY2035.

The current targets of 19% coal-fired power and 20% of LNG-fired power are insufficient as climate change countermeasures. Therefore, to fulfill its responsibilities as a developed country, Japan should revise its targets from the perspective of a complete phase-out from coal and LNG.

Furthermore, domestically, hydrogen and ammonia are expected to be “decarbonized” fuel in co-firing with coal/LNG or mono-firing in the future, and are receiving significant support from systems such as the Hydrogen Society Promotion Act and Long-term Decarbonization Power Source Auction. However, despite being promoted by government policies, the share of hydrogen and ammonia in the energy mix is expected to remain at just 0.1% and 0.2%, respectively, even by fiscal year 2035.

Japan Beyond Coal has repeatedly pointed out that hydrogen and ammonia co-firing has a small effect on emission reduction. Even based on the power generation mix forecasts, it does not seem that their use will be increased as much as the government promotes. It would be far more beneficial for energy self-sufficiency and security to redirect support and systemic measures toward renewable energy, instead of supporting hydrogen and ammonia.

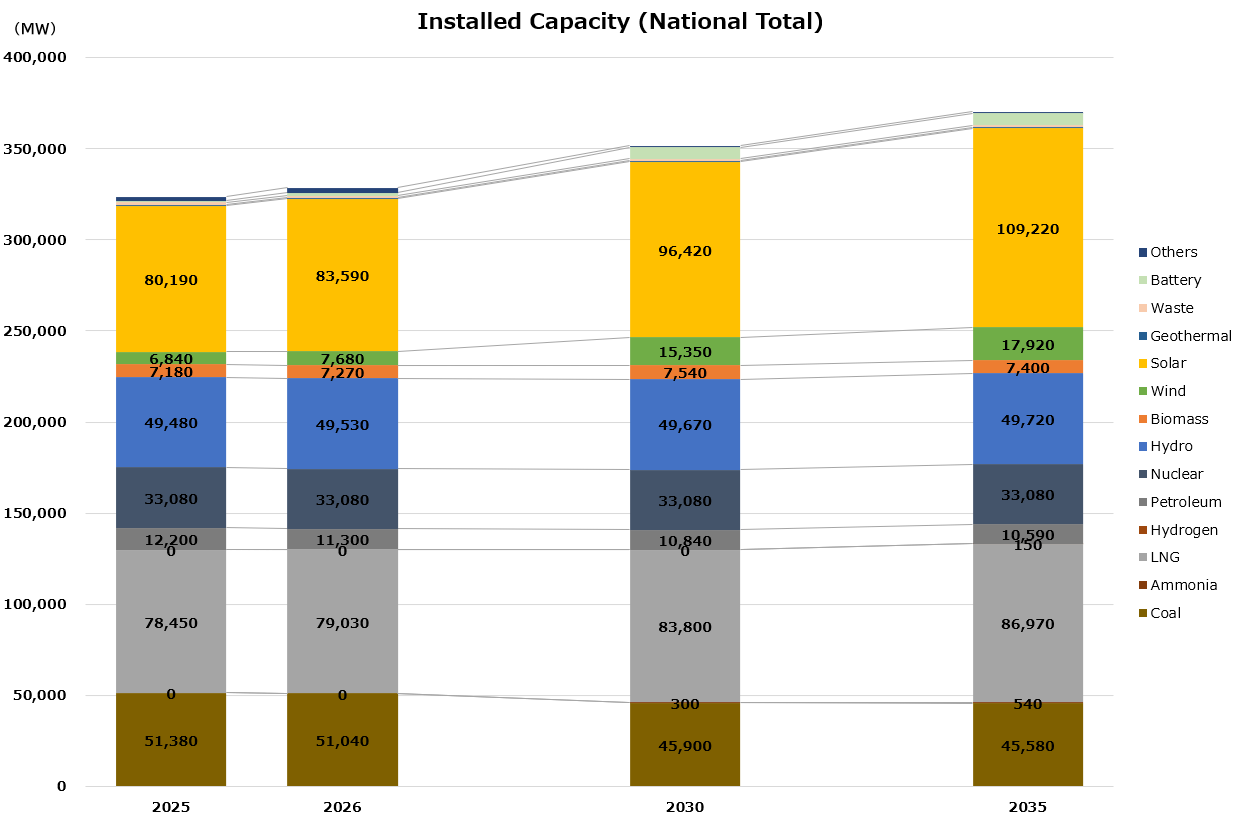

(2) Power plant capacity: Coal reduced by only 10% while LNG increases, which cancels out coal reduction efforts

The next point we should focus on is installed capacity (the amount of power generation capacity of power plants).

By FY2035, solar and wind power will lead the way in terms of growth, but LNG-fired power is expected to be the next largest increase. This contrasts with global trends, as renewable energy accounts for approximately 90% of new installed capacity.

When it comes to coal-fired power, even in FY2035 approximately 45.58 GW of installed capacity will remain, meaning that Japan is unlikely to be able to meet the international agreements mentioned in section (0).

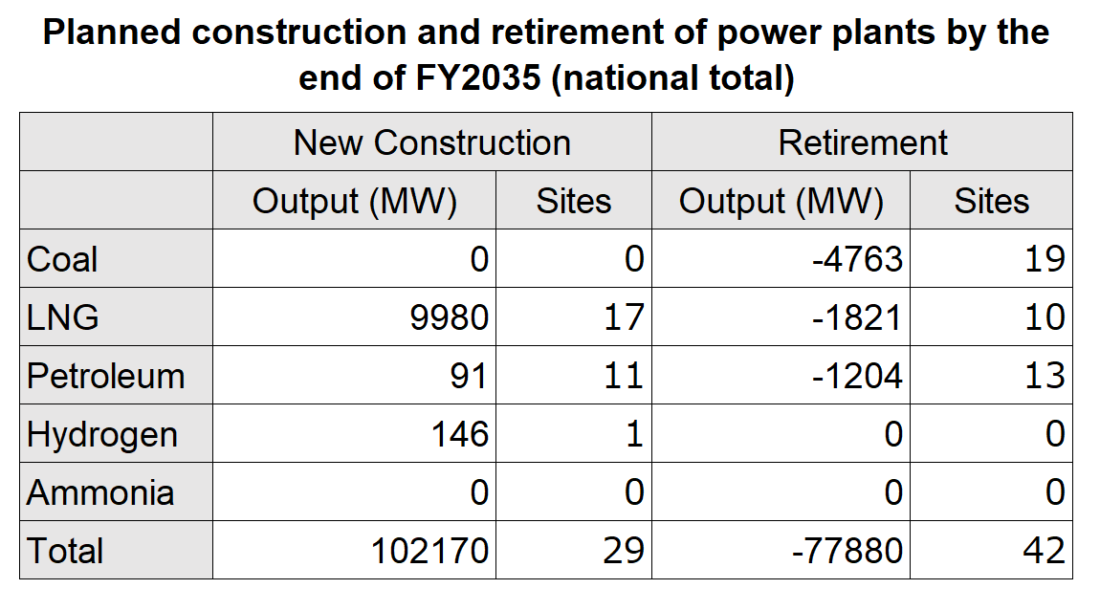

Furthermore, examining data for planned construction and retirement of power plants reveals the following.

As of April 2026, 163 coal-fired power units are operating in Japan. As mentioned earlier, in order to uphold the G7 agreement to limit global warming to 1.5℃, at least unabated old coal-fired power plants must be retired by the early 2030s.

However, the report reveals that only 10% of coal-fired power capacity is scheduled for retirement by FY2035. Moreover, the capacity of new LNG-fired power plants will exceed the reduction of coal-fired power, which results in the overall share of thermal power actually increasing. This will only worsen climate change.

Along with the plans’ announcement, OCCTO submitted an opinion addressed to the Minister of Economy, Trade and Industry (METI). It includes wording that could be interpreted as a request for a review of the government policy of “fade-out of inefficient coal-fired power plants.” As the complete “phase-out” of coal-fired power is necessary, a recommendation that even delays the phase-out of “inefficient” coal-fired power plants cannot be overlooked.

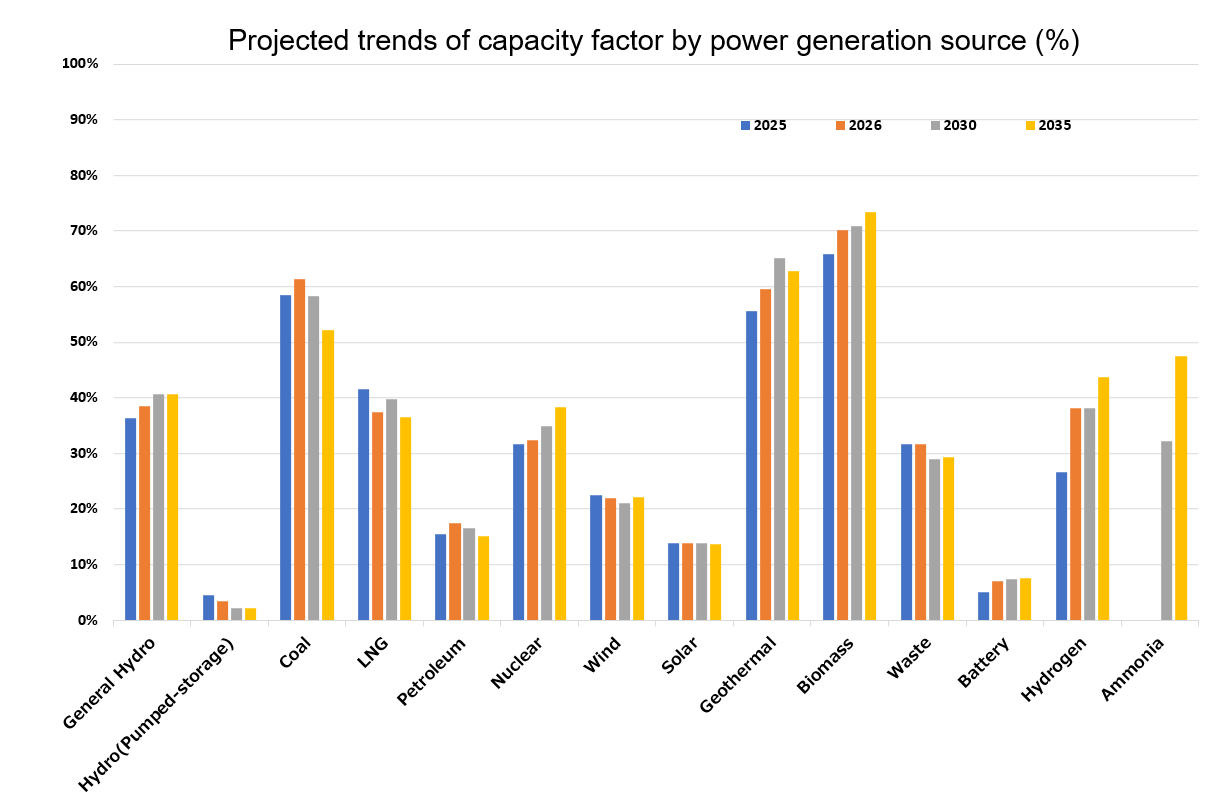

(3) Capacity factor: LNG on a declining trend, new construction as stranded assets?

While the capacity factor for coal-fired power plants has decreased by more than 15% over the past 10 years, it has remained at 57-59% in recent years.

Last fiscal year, an implementation of measures to curb capacity operations within the Capacity Market system began requiring inefficient coal-fired power plants to maintain a capacity utilization rate of less than 50%. Therefore, it was expected that the latest capacity factor for coal-fired power generation would show a decline in the overall capacity utilization.

However, instead of a decline in the overall capacity factor for coal-fired power, the FY2025 results show a slight increase compared to 2024. This may indicate either that the operation restrictions on inefficient coal-fired power plants were ineffective, or that the increase in capacity factor at other coal-fired power plants offset the declining effect. To judge the effectiveness of operation control measures, it seems necessary to compare the capacity factor of individual plants and units. Furthermore, in response to concerns over LNG supply coming from the escalating tensions in the Middle East, it has been indicated that these operation control measures will not be implemented in FY2026.

The capacity factor of LNG-fired power is gradually decreasing.

As mentioned in section (2), if the number of LNG-fired power units increases, the individual capacity factors will decrease, lowering profitability and increasing the risk of stranded assets. If construction and replacements of LNG-fired power plants are pursued to meet future surge in electricity demand, it will make emission reductions increasingly difficult and compromise achieving the Net-Zero target.

Summary

At a time of a worsening situation in the Middle East and instability of oil and LNG supply, there is an increase in support for returning to coal-fired power in Japan. However, the true shortcut to energy security is to break away from fossil fuels imports such as coal, LNG and oil. As energy security wavers due to fossil fuels, now is the time to transition from thermal power to renewable energy. Policy that requires electric power companies to review their current plans to lead to substantial emissions reductions is necessary.

Notes on this article

- This article is written based on a compilation of supply plans submitted by entities registered as electricity providers. However, based on past trends, actual results have closely followed the plans, making them a useful reference for predicting future trends. (From Kiko Network’s report “The path to 2030 based on the trends in ‘OCCTO’s aggregation of energy supply plans’” in Japanese)

- In the OCCTO compilation, hydrogen and ammonia are categorized under “New Energy etc.”, grouped together with storage batteries and renewable energy such as solar power. However, in reality, most hydrogen and ammonia are produced from fossil fuels, and categorizing them together with renewable energy is clearly misleading. Therefore, this article does not use the “New Energy” category, but lists them by source instead. (According to the IEA, as of 2023, less than 0.1% of hydrogen production comes from water electrolysis using renewable energy sources, while the rest is currently produced from fossil fuels.)