The capacity market has been criticized for prolonging the lifespan of aging thermal power plants and nuclear power plants. Not only does this system prolong the lifespan of existing thermal power plants and delay climate change measures, but it also puts the cost on the public through electricity bills. Over the course of the six main auctions held to date, the total transaction value has continued to rise and the number of power sources with bids exceeding the reference price has increased significantly. As a result, it is clear that the costs borne by the government continue to grow.

The capacity market is a mechanism distinct from the general electricity market. This is a system in which compensation is determined not by the actual buying and selling of products, but by “how much a power plant is capable of generating.” It is a mechanism to bid on and award contracts for the amount of generating capacity (in kW) that can be brought online four years from now.

If we take the case of a factory as an example, it is like the factory can receive money by merely keeping its production capability, not by selling of actual products In other words, in addition to regular electricity charges, costs associated with the capacity market will be incurred, and these costs will be borne by all electricity retailers. Although these costs are not explicitly listed on the electricity bills consumers receive, it gradually leads to higher electricity prices.

In this article, we will take a look back at the capacity market auctions, which have been held numerous times, to examine: (1) what types of power sources have been awarded contracts in the capacity market, and (2) how much money flows into the capacity market.

(1) What types of power sources have been awarded contracts in the capacity market

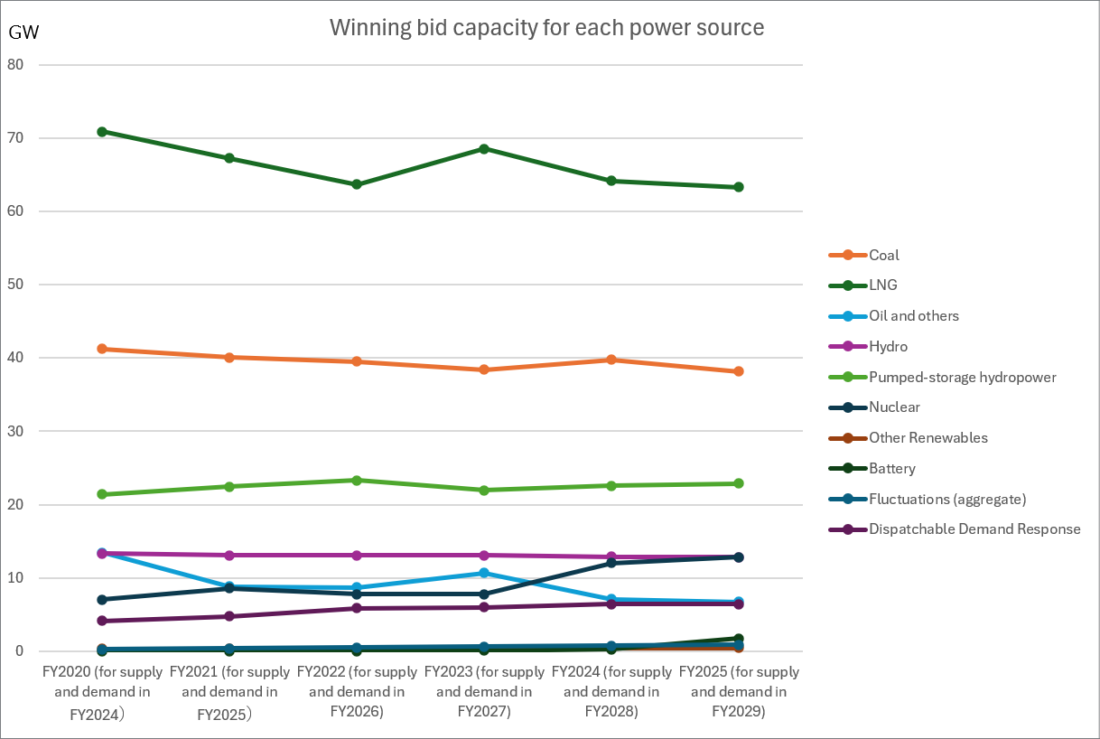

The figure below compares the capacities (in GW) of power generation facilities awarded contracts in the capacity market by power source.

*Since the volume of non-winning power sources was unknown for the first auction in FY2020,

Kiko Network used data from FY2021 onwards.

The Japanese capacity market is structured in a way that large-scale power sources, typically owned by major power utilities, frequently win bids, resulting in a consistently high proportion of LNG and coal-fired power. While the share of oil-fired power has been declining slightly, it is also notable that nuclear power has been increasing in recent years. On the other hand, renewable energy sources other than hydropower account for only a very small portion of the total, even when including variable sources (aggregators).

Coal-fired power plants are sustained by the capacity market

While coal-fired power is effectively excluded from European capacity mechanisms, the Japanese system has ended up being a structure that sustains coal-fired power.

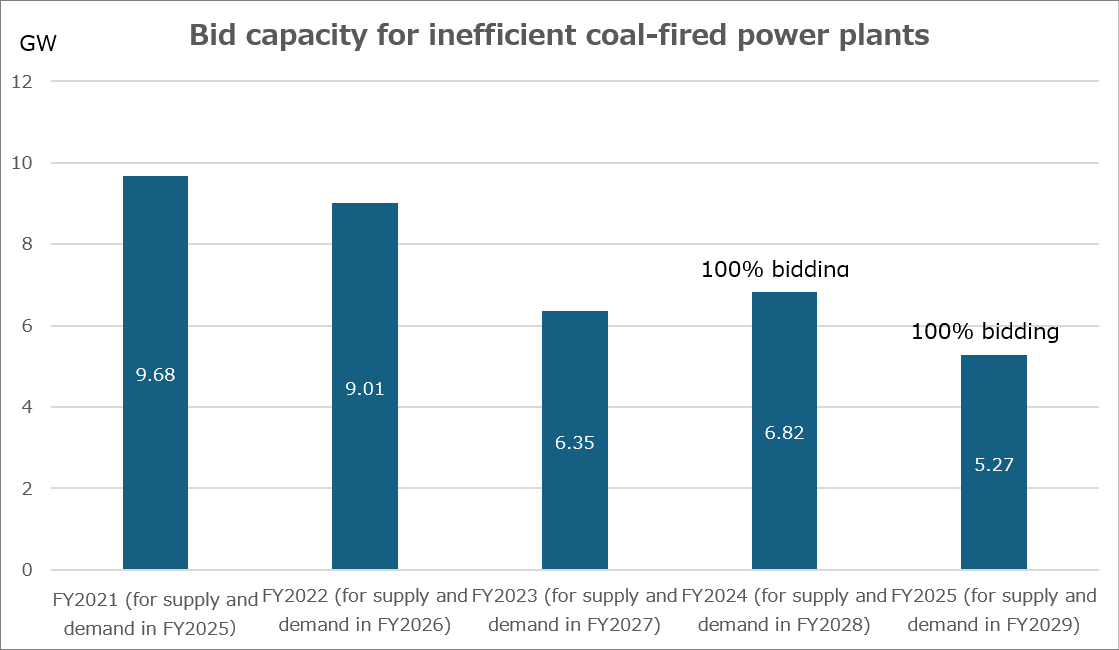

In the capacity market, to reduce the operation of “inefficient” coal-fired power, inefficient (with a generation efficiency of less than 42%) coal-fired power plants which win the bids are subjected to limit their capacity utilization rate to 50% or less, starting with the actual supply and demand for fiscal year (FY) 2025. If the targeted plant exceeds the 50% capacity utilization rate, the compensation paid to the operator will be reduced; for the FY2025 capacity market, a 20% compensation reduction was set as a penalty.

The figure below shows the bid capacity for “inefficient” coal-fired power plants for each fiscal year.

*Since the volume of non-winning power sources was unknown for the first auction in FY2020,

Kiko Network used data later than FY2021.

Looking at this trend alone, it appears that the capacity of bids is decreasing; however, this does not tell us whether inefficient coal-fired power plant is actually declining, or whether operators are taking measures—such as retrofitting—to artificially boost apparent generation efficiency and avoiding to be classified as inefficient coal-fired power. Furthermore, if this trend continues, as much as 5.27 million kW (5.27 GW) of inefficient coal-fired power, which produces high levels of CO₂ emissions, will still be in operation by FY2029.

Under the IEA’s net-zero scenario, developed countries are required to phase out all coal-fired power by 2030, and many nations are moving toward the exit of coal-fired power by that date. In contrast, Japan has not only failed to set a target year for phase-out coal-fired power but has also bidded contracts for nearly 40 million kW (40 GW) of coal-fired in the capacity market auctions held between FY2021 and 2025. If this trend continues, it will result in a serious delay in decarbonization. It is no exaggeration to say that the capacity market is structured in a way that dependence on thermal power persists.

(2) How much money flows into the capacity market.

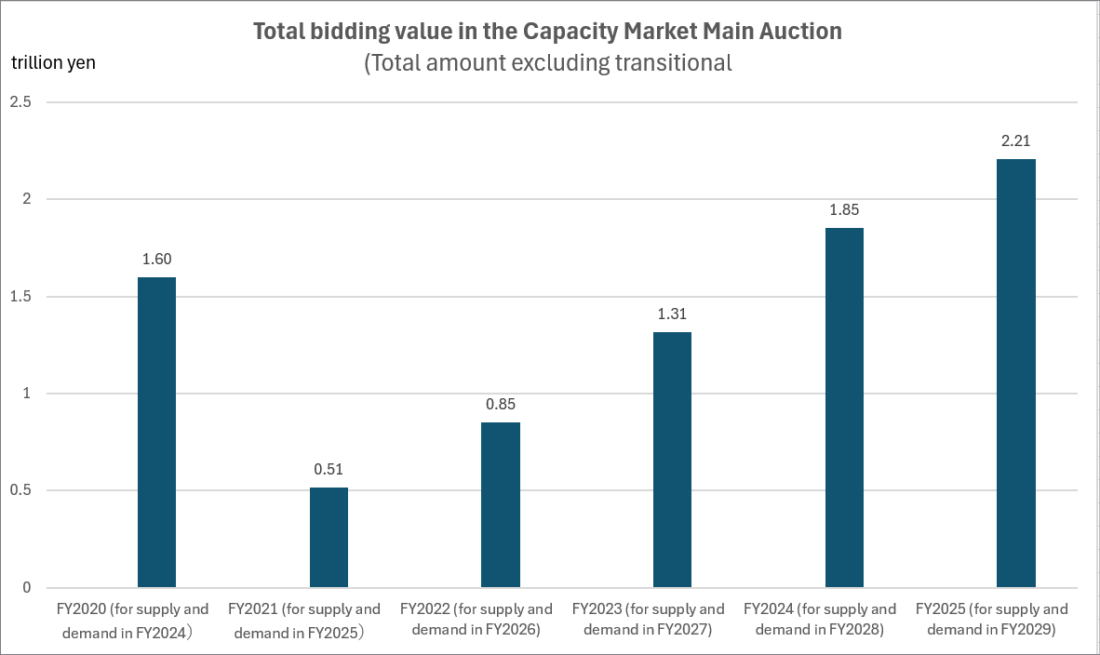

The 2025 auction reached a total of 2.21 trillion yen

It is noted that costs may remain high due to the nature of the capacity market.The figure below shows the total contract value in the capacity market (the sum of prices at which trades were executed). The council raised concern that the total contract value ballooned to 1.5987 trillion yen at the first auction and revised the bidding calculation rules. Although the total contract value declined in the FY2021 auction, it has continued to rise since then, reaching 2.21 trillion yen in the most recent auction in FY2025, significantly higher than that of the first auction. Although the total contracted capacity (kW) has remained largely flat, the total contract value has swelled to four times that of FY2021.

Why has the total contract value been increased?

The reason the total contract value has risen so sharply is believed to be the soaring maintenance and management costs of the power plants being reflected in the bid prices.

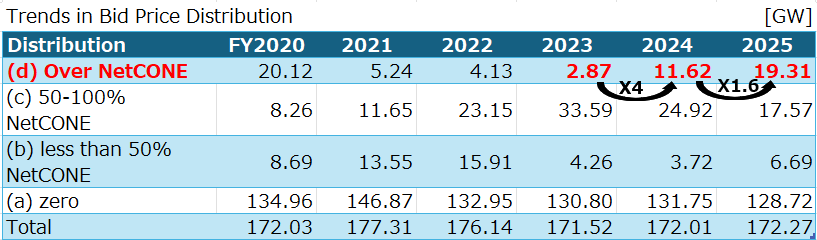

The table below shows bidding capacity by distributions for each fiscal year.

*NetCONE: NetCONE is an amount that is recovered as the cost of a new power generation capacity after accounting for wholesale and ancillary market revenues. This serves as an indicator for determining prices in the capacity market.

In recent years, the power source bidding in Category (d) Over NetCONE in the figure is considered primarily thermal power plants using LNG, oil, and other fuels. The increasing number of LNG and oil-fired power plants, which require high maintenance and management costs, is a factor driving up prices in the capacity market.

Possibility that costs in the capacity market will surge even further in the future

As costs associated with the capacity market have increased, the committee is revising measures by increasing the volume of capacity offered and the volume of bids to secure additional supply capacity in anticipation of growing electricity demand. Discussions are proceeding so that many existing power generation facilities can be successfully awarded contracts.

Table: Proposed measures to secure supply capacity in the capacity market (Based on the document of METI, prepared by Kiko Network)

| Before Bidding (Call for Bids) | Bidding | Trade Settlement | After the main auction |

| Increase in procurement volume (target procurement volume) -Demand optimization -Optimization of severe weather and low-frequency risk components -Review of additional capacity -Expected capacity of FIT-eligible power sources -Review of supply capacity planned for procurement through additional auctions -Review of projected supply capacity outside the capacity market | Maintaining and expanding bid volumes -Lowering the minimum bid volume -Considering multi-year agreements | Increase in contract volume -Revision of NetCONE ,and price cap | Measures to prevent withdrawal from contracted power supply -Review of Penalty Settings -Setting a Lower Limit on Contract Prices in Supplementary Auctions Procurement of additional supply capacity during shortages -Review of the Timing of Supplementary Auctions |

One of those revisions is the increase in the NetCONE (reference price), which is reportedly set to rise to 20,000 yen per kW—double the current rate. If the NetCONE reaches 20,000 yen per kW, LNG and oil-fired power plants that failed to win bids previously in the capacity market auctions could become eligible to win. In that case, the total contract value can be approximately 5 trillion yen.

If that happens, an increased burden on retail utilities that have to contribute funds to the capacity market will be unavoidable, and consumers may also face higher costs. These funds should be invested in expanding renewable energy and building a sustainable future. The current system, which forces consumers to continue paying high electricity rates to prop up outdated fossil fuel power plants, must be reformed.

Summary of issues regarding the capacity market

Summary points are:

- Recently, as much as 2.21 trillion yen has flowed into the capacity market, and this amount is expected to continue rising, potentially leading to higher electricity bills for consumers.

- The fact that LNG and coal-fired power plants are winning a very large number of bids in the capacity market is problematic from a decarbonization point of view.

The Japanese capacity market relies heavily on thermal power, and the committee (or government) is considering revising the system to ensure that older, existing thermal power plants can win the bids. In other countries, however, capacity mechanisms ensure future generation capacity while taking economic rationality into account, with the aim of promoting renewable energy and securing the flexibility needed to compensate for its variability. Japan must follow the lead of other countries and undertake a fundamental review of its electricity system reform.